[Income Taxes] A progressive foundation, but so much more to do

PolicyAlternatives.ca – Publications

November 1, 2019. Jennifer Robson

People with lower incomes need a say on tax reform

In recent years, calls for tax reform seem to come either from a desire to boost Canada’s competitiveness (in the hope that tax cuts will attract more foreign investment) and growth, or from a desire to increase redistribution by generating revenues to support new investment in social programs. There can be merit to both of these motivations. But either way, we shouldn’t lose sight of the effects the tax system has (or fails to have) on Canadians with low incomes.

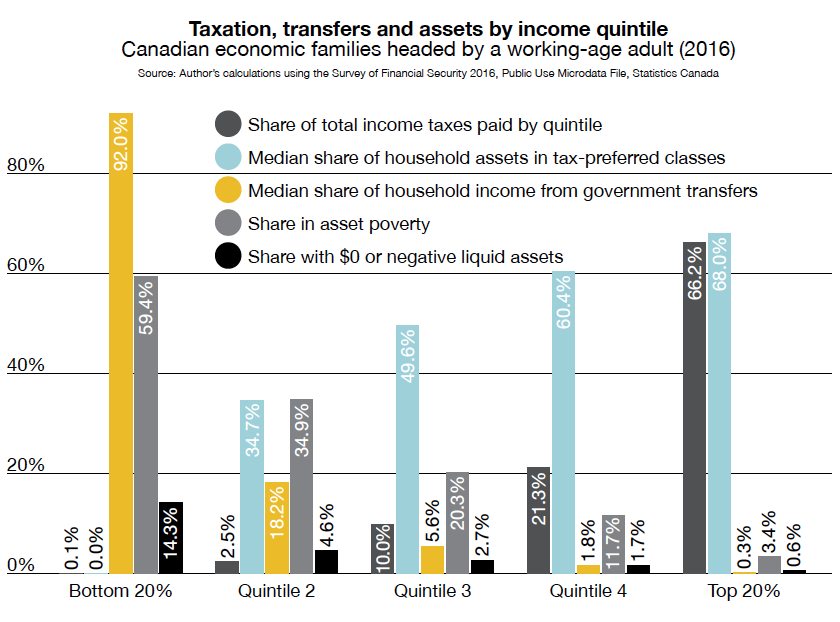

For many Canadians, the tax system can be more like a social service system. It delivers cash benefits such as the GST credit and Canada Workers’ Benefit, for example. Through a notice of assessment from CRA, the system also helps people prove their annual income so they can qualify for means-tested programs including housing and daycare subsidies, home heating rebates, and many others. In fact, working-age Canadians in the bottom quintile for market income get the vast majority of their income from government transfers, income that could be put at some risk if they can’t or don’t file a return.

For example, a low-income single mother with two children could lose as much as $13,000 if she doesn’t file a tax return to renew her eligibility for the Canada Child Benefit. In a study underway with my colleague Saul Schwartz, we estimate that 12% of adult Canadians may not file an annual tax return and could be missing out on important benefits as a result.

On the other hand, the tax and transfer system isn’t doing much to help lower-income Canadians build any kind of liquid savings. Even in the best of social insurance systems there can be gaps in coverage, and delays of weeks or even months before benefits are paid to eligible applicants. Emergency savings can make a world of difference to a family.

Nest eggs, even small ones, are also essential to investments in things like training, education and the establishment of micro-enterprises that create new and long-run opportunities for income. The current tax system provides several incentives for household savings and wealth accumulation for these and other purposes, such as exempting earnings in tax-free savings accounts (TFSAs), deductions for contributions to registered retirement savings plans (RRSPs) and favourable tax treatment when RRSPs are used for homeownership or mid-career education. The thing is, lower-income earners don’t really have access to these incentives. It’s an upside-down system that rewards people who already have money to save.

Yet Canadians at the bottom can face the double whammy of having low income to cover ongoing expenses and a small or non-existent cushion to help them cover emergencies. Fully 59% of working-age families in the bottom quintile for market income have savings too low to cover even poverty-level spending for a month; 14% of families have $0 or negative levels of liquid savings.

By contrast, working-age families in the top quintile have, at the median, just over half of their total wealth in some form of tax-benefitted asset and only a tiny share of this group are asset-poor. This figure does not even include pension assets, which can be considerable, and does not take into account preferential working-age tax deductions and tax planning to reduce taxable income in retirement.

Research by U.S. economists Emmanuel Saez and Gabriel Zucman has inspired interest in both the U.S. and Canada in creating a new annual tax on the net wealth of the very richest asset-holders. Though others have questioned its desirability and feasibility, the simple idea of a wealth tax has opened a window of opportunity to talk about broader issues of tax fairness, and how tax and transfer systems shape the financial security (or precarity) of Canadian households.

Here are a few examples of the kinds of policy directions that could be brought forward in any conversation about tax reform. All of them have the potential to make a meaningful difference in the financial well-being of lower-income Canadians.

Embrace automation in the tax system

In the 2018 federal budget, the government announced that the Canada Workers’ Benefit (formerly the Working Income Tax Benefit) would no longer need an application on top of an annual income tax return. Instead, CRA would now automatically assess returns for eligibility for the refundable tax credit. A similar auto-enrolment measure has also been introduced for the Guaranteed Income Supplementpayable to lower-income seniors.

These changes are important. But moving to pre-filled tax forms or even return-free filing would do far more to ensure that tax-filing is no longer an obstacle to accessing means-tested programs and benefits. The transformation—from self-assessed to government-assessed tax-filing—could be extended to all Canadians, not just those with low incomes and simple returns. Of course, that would only be possible if we also simplified the overall system, reducing the many assorted credits that demand self-reporting and self-assessment.

Make emergency savings real for everyone

Right now, the tax treatment of savings and assets offers multiple avenues for those with higher incomes to reduce their taxes owing by investing in certain kinds of assets. For those with low or no tax liability, these incentives do almost nothing to reward their savings. Worse still, clawbacks on means-tested benefits such as the Guaranteed Income Supplement can mean that low-income savers are severely penalized if they pick the wrong kind of asset for their modest savings.

An income-tested and refundable credit could provide an incentive to lower-income savers that would complement the existing tax savings offered to higher-income savers. If tied to a TFSA, which still badly needs a lifetime contribution limit, a refundable credit would make it easier for so-called small savers to build a bit of a nest egg to cover short-term emergencies or longer-term needs.

Rationalize non-refundable tax credits

If we can’t quite shake our collective love of boutique tax credits, we can at least look for opportunities to streamline the tax code where refundable credits would be more effective. For example, the non-refundable Canada Employment Credit effectively provides a maximum $179 credit against federal taxes owing for persons with employment income. But the program costs roughly $2.5 billion per year and has no clear impact on labour force participation. For the same amount of money we could double the refundable Canada Workers’ Benefit, encouraging increased employment and reducing poverty among working-age Canadians.

When we talk about tax reform it can be easy to overlook lower-income Canadians, since they are less likely to be net payers on personal income taxes. But the tax system is more than just a public revenue system: for many lower-income Canadians, it is a key part of how they get the income and benefits they need. They need a voice in tax reform too.

Jennifer Robson is Associate Professor of Political Management at Carleton University.

https://www.policyalternatives.ca/publications/monitor/progressive-foundation-so-much-more-do?mc_cid=b73f32de93&mc_eid=26a8b9335a

Tags: economy, ideology, participation, poverty, standard of living, tax

This entry was posted on Friday, November 1st, 2019 at 2:56 pm and is filed under Governance Policy Context. You can follow any responses to this entry through the RSS 2.0 feed. You can skip to the end and leave a response. Pinging is currently not allowed.

Leave a Reply

Recent Comments

Recent Comments